Asaan Karobar Finance Scheme .The Government of Punjab has always been keen to open ways for economic empowerment of its people. In this context, various efforts have been made to provide entrepreneurial opportunities, self-reliance, and sustainable growth. These include the Asaan Karobar Finance Scheme (AKFS), which has been a path-breaking initiative for promoting small businesses, new entrants, and self-employment. Now, with the launch of Phase-2, the scheme is ready to empower more individuals by expanding financial access and convenient financing opportunities in all nooks and crannies of Punjab.For this article, the objectives, salient points, benefits, eligibility, and larger aspects of the Asaan Karobar Finance Scheme Phase-2 are discussed while foregrounding why the scheme is a landmark in the socio-economic history of the province.

Table of Contents

Background of the Asaan Karobar Finance Scheme

The Asaan Karobar Finance Scheme was launched for the first time as part of Punjab’s vision to grow small and medium enterprises (SMEs). The scheme identifies the role of small firms as the backbone of the economy, playing the role of employment generation and overall GDP growth.

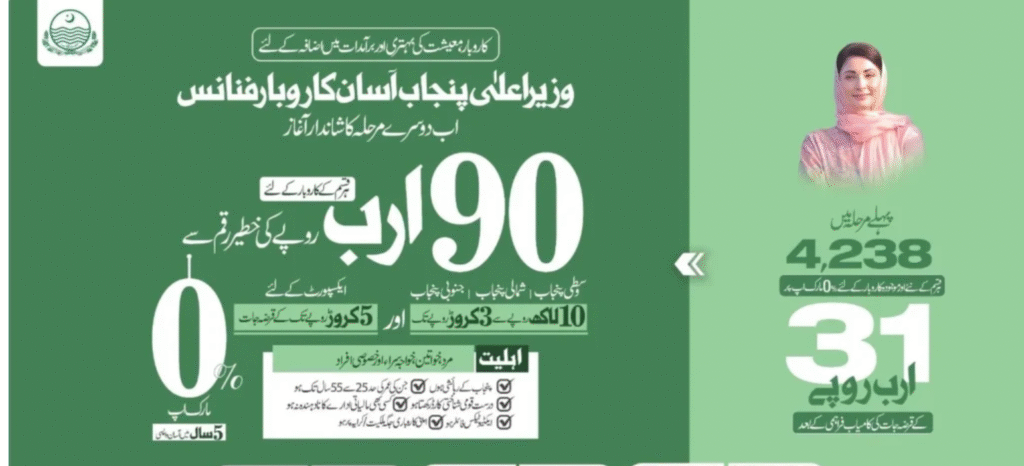

In its Phase-1, the scheme had been able to offer inexpensive financing to thousands of people who could not obtain a loan from the traditional banks because of issues of collateral or strict terms. By providing soft terms, lower interest rates, and simple paperwork, the scheme promoted entrepreneurship and improved the welfare of many families. Emboldened by this achievement, the administration decided to increase the scheme to Phase-2 with enhanced features of inclusivity, larger financial outlays, and wider spread across un-served areas.

The Phase-2 Rollout of the Asaan Karobar Finance Scheme has been planned with several objectives in mind:

Key Targets of Phase-2

You May Also Promote Entrepreneurship: Empowering the youth and women of Punjab to be entrepreneurs with no hassle.

💼Enable Self-Employment: Offering chances to freelancers, small shopkeepers, and professionals to initiate or grow their enterprise.

🌍Inclusive Growth: Facilitating greater access to finance to the disadvantaged groups like women, minorities, and rural residents.

👷Job Generation: Empowering small businesses that, in turn, create job opportunities for others.

📈Economic Stability: Improvement of economic growth in Punjab through strengthening grassroot enterprises and curbing dependence on foreign borrowing.

Features of Phase-2

The Asaan Karobar Finance Scheme Phase-2 unveiled some new features to enhance the program effectiveness:

💰Loan Amounts: Loan facilities ranging from PKR 100,000 to PKR 2 million as per the size of business and requirement.

.

📅Installments within 3-5 years for convenient repayment.

🏦Interest-free or low-markup funding: Certain groups are extended interest-free loans, and others have access to highly subsidized markup terms relative to business loans.

🛡️Collateral-free loans: Loans are provided to most applicants without collateral requirements, making it particularly well-suited for first-generation entrepreneurs.

👩💼👨🎓Women & Youth Priority: A significant quota has been set aside for women entrepreneurs and youth graduates.

💻Electronic Application Process: Online applications by applicants eliminated paperwork and introduce transparency.

🛍️Sectoral Coverage: Ranging from retail shops, tailoring units, and IT start-ups to agriculture-related businesses, the scheme has wide coverage of enterprises.

Eligibility Criteria of Asaan Karobar Finance Scheme

To promote justice and inclusiveness, the Phase-2 eligibility criteria are simple:

1.Residence Requirement: Applicant should be a Punjab resident.

2.Age Requirement: Generally between 18 to 50 years.

3.Eligibility for All: Both male and female are eligible to apply.

4. Business Idea/Plan: Applicant should provide a viable business idea or plan.

5.Already Running Companies: Small companies already running and seeking expansion are also applicable.

⭐ Special Preference: Educated youth, women, minorities, and differently-abled will be preferred.

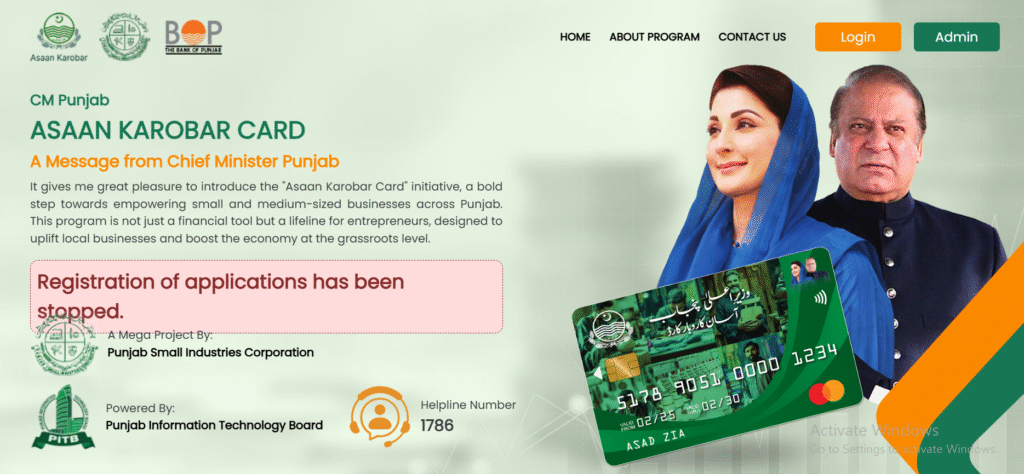

Visit:https://www.punjab.gov.pk/asaan-karobar-financeApplication Process

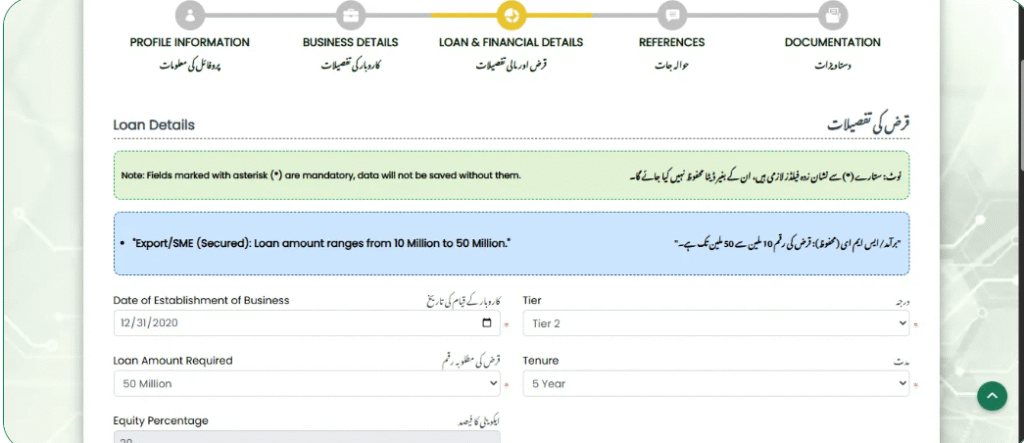

Online Registration: Candidates log in at the Punjab government website or bank’s specific website

Form Submission: Personal information, CNIC data, and business proposal are completed.

Verification: Application is screened and appropriateness verified by banks and government officials.

✅ Approval & Disbursement: Upon approval, the loan is credited to the applicant’s account directly.

Monitoring & Support: Candidates may also be provided with business counseling and training seminars.

Scheme advantages

🏦Financial Inclusion: It awakens those who were earlier outside the purview of the formal financial system.

🚀Start-up Motivation: With a negligible or no collateral requirement, new start-ups can make their initial entry without fear of finance.

👩💼Women Empowerment: Exclusive quotas for women provide them with an equal business chance.

🛠️ Reduction in Unemployment: By motivating self-employment, the scheme directly helps in lessening joblessness.

👥Economic Push: Better local business activity enhances the overall economic progress.

📈Skill Development: Tailors, barbers, carpenters, IT professionals, and artisans are now able to open their businesses with lesser hindrances.

Impact on Punjab’s Economy

Better SME Sector: Easier finance will help small and medium businesses expand several times in size.

Rural Development: With loans in villages and small towns, the scheme fills the urban-rural economic divide.

Export Potential: IT startup promotion and agriculture business may contribute to the export potential of Punjab.

Poverty Alleviation: With higher earning prospects, families are able to bridge over over the poverty line.

Challenges and Solutions

Awareness Gap: Most people, particularly rural dwellers, do not know about the scheme.

Loan Recovery Issues: Default chances are high in case businesses fail.

Capacity Building: Entrepreneurs are ill-equipped to do business.

Future Prospects

The Asaan Karobar Finance Scheme Phase-2 provides the foundation for a prosperous economic future. Executed properly, it can turn Punjab into a commercial hub of small business entrepreneurship. Through technology-based apps, transparent processes, and state-funded assistance, the scheme can be a model initiative for the other Pakistani provinces.

And visit:Kisan Dost Scheme 2025–26: Government Support for Farmers in Pakistan

Conclusion

Asaan Karobar Finance Scheme (Punjab) Phase-2 Launch is not only a finance scheme, but a pending socio-economic revolution. Empowering the masses, encouraging self-employment, and financing SMEs, the scheme is an inspiration to thousands of young entrepreneurs.Punjab government has rightly realized that economic self-sufficiency can be achieved by encouraging small enterprises. Phase-2 is going to make significant contributions towards opportunity creation, unemployment reduction, and inclusive growth for all.

Essentially, the scheme is not just a money-making programme – it is a move in the direction of bringing to realization a self-sustaining Punjab where every citizen can dream, toil, and prosper.

What is the Asaan Karobar Finance Scheme (Punjab)?

The Asaan Karobar Finance Scheme is a government initiative launched to support small businesses, startups, and self-employed individuals in Punjab. It provides easy loans with flexible repayment plans to promote entrepreneurship and reduce unemployment.

What is new in Phase-2 of the Asaan Karobar Finance Scheme?

In Phase-2, the scheme has been expanded with higher loan limits, digital applications, women quotas, and more inclusive coverage for rural and urban businesses. It also offers better repayment terms and wider sectoral support.

Who is eligible for the Asaan Karobar Finance Scheme Phase-2?

Any resident of Punjab between 18 and 50 years of age can apply. Both men and women are eligible, with special priority for youth, women entrepreneurs, minorities, and differently-abled individuals.

How much loan can I get under Phase-2 of the scheme?

Applicants can avail financing from PKR 100,000 to PKR 2 million, depending on their business type, plan, and requirements.

Is collateral required for the Asaan Karobar Finance Scheme?

Most loans under Phase-2 are collateral-free, especially for first-time applicants. However, larger loans may require minimal security depending on the applicant’s profile.